“This article has been produced in association with our lawyers and specialist asset protection and estate planning advisers, Abbott & Mourly”

Introduction

Building Family Wealth takes time, hard work and a lot of blood, sweat and tears. But it can be torn down so easily in expensive litigation, legal challenges plus regulatory and economic threats. It is not unheard of for a $1M deceased person’s estate to be challenged and when that happens expect upward of $200,000 in legal fees and years of litigation. The bigger the estate the larger the fees. And anyone with a business or profession, from a doctor advising patients to a property developer with their latest project to a hairdresser who may have spread Covid to clients, they may be exposed to lengthy and costly lawsuits.

This does not have to happen!

Family Wealth - Is Yours Protected?

There are five ways that family wealth can be attacked – each a potential time bomb on a family’s wealth and health.

(i) Litigation

We are living in an era where our employees, children, spouses, neighbours, government, councils, tenants and regulators can sue you and there is no end of No Win No Fee lawyers ready to take up the case. You may not know it, but Australia produces more law students per capita than any other nation on earth. That is why Australia has a very strong legal industry that earns more than $23Bn in revenue each year and even managed investment vehicles enabling investors to pool money together to invest in class action litigation. EXPOSED: Assets of any kind in your own name are exposed in a litigation action. The biggest threat is not the litigation, but the time taken in the legal system, the stress and the sheer amount of legal fees that can easily escalate in any litigation.

(ii) Incapacity

Where a person suffers from mental incapacity then they cannot be a trustee or director of a company. And what we have learned with Covid, is that a medical event can put a person out of action for some time. • What happens if they are the sole director or a director of a trustee company for a discretionary trust or a SMSF? • Who is going to run the show? Without any strategic solution put in place prior to the incapacity, any business, trust, super fund or investment is at peril as the family wealth ship cruises into unchartered waters without a captain or rudder. EXPOSED: Assets, investments, companies, trusts, super funds are exposed where a key person, director or trustee become incapacitated.

(iii) Bankruptcy

For many business owners and professionals Covid has had an impact on their income and the strength of their business or career. We are moving into unchartered waters and many insolvency practitioners are talking about the significant uptick in their business – at the expense of family wealth. It is heartbreaking to see family businesses go to the wall through government lockdowns and actions with no protection in place. EXPOSED: Assets, investments, companies, trusts and even superfunds are exposed where a key person, director or trustee is in the throes of insolvency or bankruptcy.

(iv) Death

On death most people who have a Will would expect that all of their personal assets, including home, investments and superannuation would be paid out in accordance with their Will. Wrong!!! Every State in Australia allows a disaffected person (someone who did not benefit from a Will or obtain what they believe they deserved) to claim against an estate. Any claim overrides the provisions of a Will. A Real Case in Point: A family provision claim on estate assets may result in long and costly court proceedings. In Western Australia in 2018 the judge of the WA Supreme Court castigated lawyers who had taken five years and $500,000 in legal fees to challenge a $600,000 estate consisting only of the deceased’s home. This is happening every day in Supreme Courts around Australia and that should not happen to you. Your choice of what to do with your family’s assets should be your choice, not the choice of a Supreme Court judge looking for the person who needs the assets. EXPOSED: Assets, investments, companies, trusts, super funds are exposed to family provisions litigation where a key person, director or trustee dies.

(v) Family Law

Most people are not aware that a simple de-facto relationship that has lasted two years means both parties of the relationship, in the event of a relationship breakdown, have full recourse against the other’s property under the Family Law Act in Australia. Giving adult children money, inheritances, help with purchasing a property, or having an unpaid present entitlement in a family trust may add fuel to the fire in a relationship breakdown. The same with marriage and more so, with second and third marriages. The old asset protection strategy of putting assets in a spouse’s name to protect from litigation can be a disaster in the making from a Family Law perspective. EXPOSED: The Family Law Court has supreme powers to split all assets, investments, companies, trusts and super funds in a relationship breakdown.

Solution - The Protector

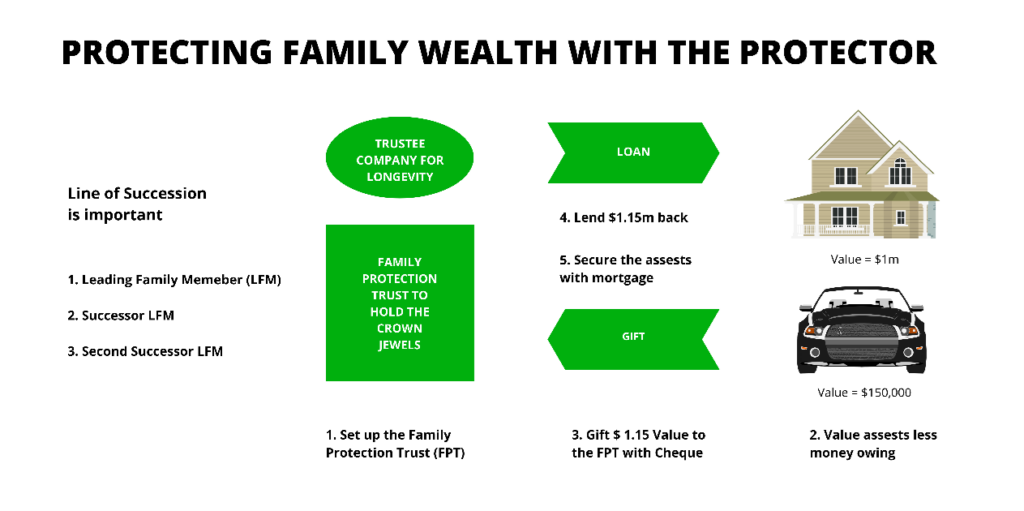

Lawyers and specialist asset protection and estate planning advisers, Abbott & Mourly have developed “The Protector”, a family wealth protection package, which available to us at Concepts & Results, which not only provides asset protection, but ensures that your assets are held for the benefit of those beneficiaries in your lineage or bloodline that you want. This will ensure that your assets are kept in the hands of your lineage.

Diagram One shows how the Protector works graphically.

In Part Two of our Guide to Family Wealth Protection we review each of the steps and why they are important. Also while on our site, check out our succession, asset protection and estate planning services.